Does a strong regulatory framework decrease malfeasance in accounting?

Scandals that rocked the South African account profession

The WOW report on the accounting sector in South Africa highlights the scandals that rocked the accounting profession in recent years. Such disgraces always get the limelight, sometimes rightfully so even though at times the wider context is overlooked. This is because of the role the sector plays in guiding businesses; the profession is thus expected to hold high moral standards. History has shown that regulation in the accounting sector is necessary given the great influence of the accounting practice on people’s behaviour and the impact on lives and organisations.

One of the biggest accounting firms Arthur Andersen, which had offices in South Africa, was found guilty in 2002 in the US for shredding evidence and lost its licence to engage in public accounting. Arthur Andersen was Enron’s auditor and consultant up to Enron’s bankruptcy filing in 2001. Arthur Andersen had advised on (dubious) schemes that they vetted and accepted in the financial statements. As we know, the Enron bankruptcy saw investors and employees lose billions of dollars, and several Enron executives went to jail. That had a huge knock on the accounting sector in general.

The cost of regulation

Importantly, the scandals resulted in a wave of new regulations and legislation designed to increase the accuracy of financial reporting for companies. To comply with new regulations requires training as well as a change of culture and processes, imposing costs felt mostly by smaller players.

How is it that new regulations which reverberated throughout the world, mainly for big accounting firms, did not prevent what happened in South Africa recently with Steinhoff (R106bn potential losses) or in Germany with Wirecard (R1.9bn) which were shielded by inadequate auditing and reporting by accounting firms.

Nevertheless, a balanced approach is required. This is the theme of Cass Sunstein in his book Laws of Fear: Beyond the Precautionary Principle. In his view, “people will be very familiar with the losses associated with new risk, or those aggravated by existing risk, but far less concerned with the benefits that are foregone as a result of regulation’.

Generally, people overestimate the low probability of certain adverse events. Sunstein states that the overreaction to adverse events also applies to government and law under the same circumstances. This leads to estimates of consequences being exaggerated followed by overregulation at a high cost, exceeding foregone benefits, when the possibility of such adverse events sometimes is very low and such regulation likely not able to prevent the events it is supposed to eliminate.

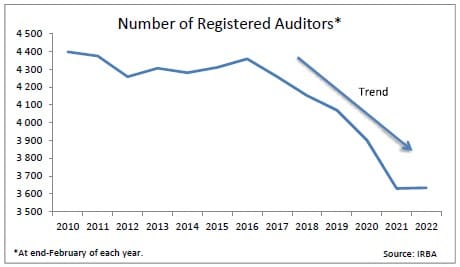

A practical example, mentioned in the WOW report, is that of the Independent Regulatory Board for Auditors (IRBA) which found it necessary to increase compulsory membership fees to such an extent that the East Rand Member District took it to court. The professional body also claimed that IRBA’s financial management was not up to standard.

This led to a decline in membership and plunged the auditors’ profession in South Africa into disarray due to the high input costs triggered by the 35% IRBA fee hike and the perceived increased risks associated with exercising auditing. The graph below paints a picture of the registered membership decline, which raises a red flag.

The economic context

It is important to note that the scandals were found out, not due to regulation, but by the media which has exposed corruption and is holding leaders to account. A repeat of such instances does not become entirely avoidable by excessive costly overregulation.

All in all, the percentage of fraud casualties of JSE-listed companies is relatively small compared to the corruption in the public sector. Imagine for a second if 70% of JSE-listed companies would receive qualified audits.

It is important to note that the malfeasances in the private sector had real felt consequences in wealth destruction for investors. In the public sector such wealth destruction, as in reduced services, is diluted across the entire population who cannot elect not to invest in a particular public service.

Impact of regulation in the South African public sector

The Auditor-General has been armed with more regulatory authority, but the wrongdoing has continued without strong sanctions. As demonstrated over the years in the South African public sector, all regulation comes to nothing if there is no consequential action taken.

Year in and year out, the Auditor-General issues qualified audits and highlights unauthorised and wasteful expenditures and fraud as well as corruption at all levels of government and within the SOEs, with the aim of alerting them to areas in need of improvement, but no serious concomitant remedial action is taken.

This calls for the government and its regulators to bear this dichotomy in mind when considering further regulation and rather devote more attention to detailing and legislating impactful consequences for impactful corruption such as bid rigging in the procurement processes.

Contact us to access WOW's quality research on African industries and business

Contact UsRelated Articles

BlogCountries Financial and insurance activitiesSouth Africa

Cryptocurrencies and security dealing activities in South Africa

Contents [hide] The main players in securities dealings and South Africa’s position The rise of cryptocurrencies has introduced new dynamics in securities dealing, challenging traditional financial markets and regulatory frameworks....

BlogCountries Financial and insurance activitiesSouth Africa

The development of flexible and customised insurance products in South Africa

Contents [hide] Life insurance as a business Life insurance is unlike many other businesses in that it has an uncertain future cost associated with the income it generates from premiums,...

BlogCountries Financial and insurance activitiesSouth Africa

The rise of new competition in the South African banking sector

Contents [hide] The financial services sector in South Africa stretches from the South African Reserve Bank to micro lenders, cooperative banks, stokvels and loyalty programmes that have become popular for...